Tokyo, 27 December, /AJMEDIA/

1. On December 27, “Convention between Japan and the Republic of Azerbaijan for the Elimination of Double Taxation with respect to Taxes on Income and the Prevention of Tax Evasion and Avoidance (hereinafter referred to as the New Convention) (English (PDF) / Japanese (PDF)) was signed in Baku, the capital of Azerbaijan by H.E. Mr. WADA Junichi, Ambassador of Japan to the Republic of Azerbaijan and H.E. Mr. Mikayil Jabbarov, Minister of Economy of the Republic of Azerbaijan.

2. The New Convention wholly amends the existing Convention (Convention between the Government of Japan and the Government of the Union of Soviet Socialist Republics for the Avoidance of Double Taxation with respect to Taxes on Income), which entered into force in 1986, between Japan and the Azerbaijan, mainly by revising the taxation on business profits, expanding the extent of reduction of taxation on investment income, as well as by introducing measures for prevention of abuse of the New Convention and assistance in the collection of tax claims, and by reinforcing the exchange of information concerning tax matters. It is expected that, while eliminating double taxation and preventing international tax evasion and tax avoidance, the New Convention promotes further mutual investments and economic exchanges between the two countries.

3. The following are the key points of the New Convention.

(1) Taxation on Business Profits

Where an enterprise of one of the two countries has in the other country a permanent establishment (such as a branch, including the furnishing of services by an enterprise through personnel over a certain period of time) through which the enterprise carries on business, only the profits attributable to the permanent establishment may be taxed in that other country. The profits attributable to a permanent establishment will be calculated by comprehensively recognizing internal dealings between its head office and branches and by strictly applying the arm’s length principle.

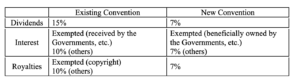

(2)Taxation on Investment Income

Taxation on investment income (dividends, interest and royalties) in the source country will be subjected to the reduced maximum rates or exempted as follows:

(3) Mutual Agreement Procedure

Taxation not in accordance with the provisions of the New Convention may be resolved by mutual agreement between the tax authorities of the two countries.

(4) Exchange of Information and Assistance in Collection of Tax Claims

In order to effectively prevent international tax evasion and tax avoidance, the scope of taxes and cases subject to the exchange of information concerning tax matters is expanded and the mutual assistance in the collection of tax claims between the two countries is introduced.

(5) Prevention of Abuse of the New Convention

In order to prevent abuse of benefits under the New Convention, any benefit under this the New Convention will not be granted if it is reasonable to conclude that obtaining such a benefit was one of the principal purposes of any transaction, or if the income is attributable to a permanent establishment in a third country and does not satisfy specified conditions.

4. After the completion of the domestic procedures in each of the two countries (in Japan, approval by the Diet is necessary), each of the two countries shall send through diplomatic channels to the other country the notification confirming the completion of its internal procedures. The New Convention will enter into force on the thirtieth day after the date of receipt of the latter notification and will have effect:

(a) in Japan:

(i) with respect to taxes levied on the basis of a taxable year, for taxes for any taxable years beginning on or after 1 January in the calendar year next following that in which the New Convention enters into force; and

(ii) with respect to taxes levied not on the basis of a taxable year, for taxes levied on or after 1 January in the calendar year next following that in which the New Convention enters into force; and

(b) in Azerbaijan:

(i) with respect to taxes withheld at source, for income derived on or after 1 January in the calendar year next following that in which the New Convention enters into force; and

(ii) with respect to other taxes, for taxes chargeable for any fiscal year beginning on or after 1 January in the calendar year next following that in which the New Convention enters into force; and

(c) The provisions concerning the exchange of information and the assistance in the collection of taxes have effect from the date of entry into force of the New Convention without regard to the date on which the taxes are levied or the taxable year to which the taxes relate.

* The New Convention will not affect the application of the current Tax Convention (Convention between the Government of Japan and the Government of the Union of Soviet Socialist Republics for the Avoidance of Double Taxation with respect to Taxes on Income) between Japan and some of the former Soviet Union countries other than Azerbaijan.